This article is not approved yet.

Photo By: Kaboompics.com: https://www.pexels.com/tr-tr/fotograf/kisi-yazmak-yazi-oturmak-5900184/

Cost-Volume-Profit (CVP) Analysis

Who is İt for? | Managers, entrepreneurs, finance students | ||||||||

|---|---|---|---|---|---|---|---|---|---|

Key Elements | sales price contribution margin variable costs Fixed costs | ||||||||

Why Use İt? | Support pricing & production decisions Analyze profit potential Find break-even point | ||||||||

What is İt?? | A financial tool that shows how cost, sales volume, and profit interact. | ||||||||

Cost-Volume-Profit (CVP) Analysis

A basic financial analysis technique that aids companies in comprehending the connection between expenses, sales volume, and profit is cost-volume-profit (CVP) analysis. As a strategic tool, this approach is particularly crucial for managers and decision-makers. Businesses can use CVP analysis to determine how many units they need to sell at a specific pricing and cost structure in order to turn a profit and prevent losses. It finds the crucial balance between income and expenses and depends on differentiating between fixed and variable costs. In this way, CVP research serves as a foundation for creating price plans, streamlining cost structures, and forecasting profitability for future planning.

CVP analysis is based on three key elements: sales income, variable costs, and fixed costs. Rent, salary, and insurance are examples of fixed expenditures that don't alter based on the volume of production. Conversely, variable costs—such as commissions, direct labor, and raw materials—change in response to the volume of production or sales. The number of units sold multiplied by the unit sales price yields the sales revenue. Analyzing a company's financial success requires an understanding of how these elements interact.

The difference between the unit variable cost and the unit selling price is known as the contribution margin. It is utilized to pay for fixed expenses, and any surplus over those expenses is turned into profit. For instance, the contribution margin is €1.80 per unit if a product is sold for €4.00 and the variable cost is €2.20. This sum is the profit per unit before fixed costs are subtracted.

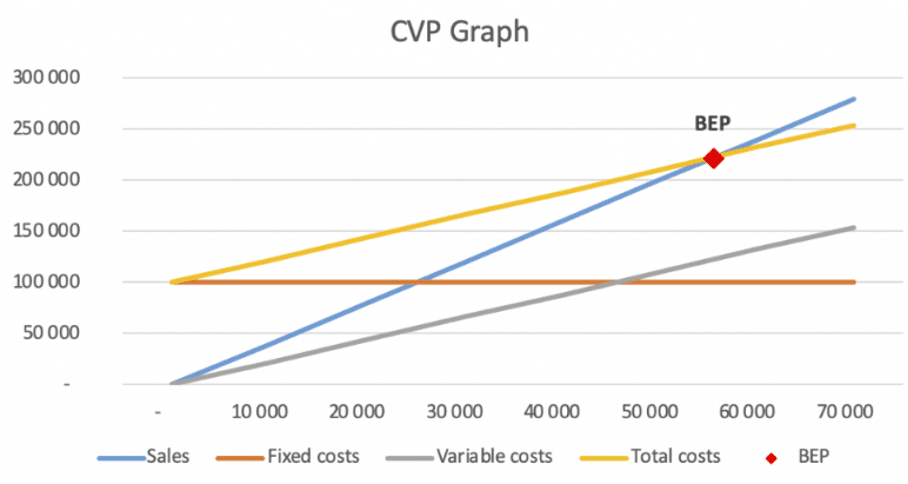

The break-even point is where total revenue equals total costs, resulting in neither profit nor loss. In CVP analysis, the break-even point is calculated by dividing total fixed costs by the contribution margin:

Break-Even Volume = Fixed Costs / Contribution Margin

CVP analysis allows businesses to calculate expected profit under different sales volumes using the following formula:

Profit = (Selling Price × Units Sold) − (Variable Cost × Units Sold) − Fixed Costs

This formula helps managers predict the impact of sales volume changes on profitability and supports financial planning decisions.

CVP analysis is not limited to profit/loss evaluation. It also guides pricing decisions, product portfolio management, new product investment strategies, cost reduction initiatives, and risk management. With this method, businesses can identify their most profitable products, align production plans accordingly, and base financial goals on solid foundations.

Cost-Volume-Profit Analysis Graph

AccountingProfessor.org. (n.d.). Everything you need to know about cost-volume-profit (CVP) analysis. Retrieved July 4, 2025, from https://accountingprofessor.org/everything-you-need-to-know-about-cost-volume-profit-cvp-analysis/

Ansari, A., & Qureshi, M. A. (2023). Break-even analysis: A tool for managerial decision-making. PNR Journal, 8(3), 112–119. https://www.pnrjournal.com/index.php/home/article/view/4490/4906

Ficcadenti, V., Mazzocchetti, A., & Benedetti, M. (2023). Optimization of production planning using cost-volume-profit analysis. PLOS ONE, 18(11), e0294623.

Karthikeyan, M., & Saranya, R. (2023). Analysis of break-even point in business decision using CVP. International Journal of Management and Entrepreneurship, 15(1), 85–92. https://techmindresearch.org/index.php/ijme/article/view/940/582

Magnimetrics. (2020, November 26). Cost-volume-profit analysis & break-even point. Retrieved July 4, 2025, from https://magnimetrics.com/cost-volume-profit-analysis-break-even-point/

Photo By: Kaboompics.com: https://www.pexels.com/tr-tr/fotograf/kisi-yazmak-yazi-oturmak-5900184/

Cost-Volume-Profit (CVP) Analysis

Who is İt for? | Managers, entrepreneurs, finance students | ||||||||

|---|---|---|---|---|---|---|---|---|---|

Key Elements | sales price contribution margin variable costs Fixed costs | ||||||||

Why Use İt? | Support pricing & production decisions Analyze profit potential Find break-even point | ||||||||

What is İt?? | A financial tool that shows how cost, sales volume, and profit interact. | ||||||||

No Discussion Added Yet

Start discussion for "Cost-Volume-Profit (CVP) Analysis and Break-Even Analysis" article

Key Concepts

Contribution Margin

Break-Even Point

Profit Calculation

Strategic Importance

Limitations

This article was created with the support of artificial intelligence.